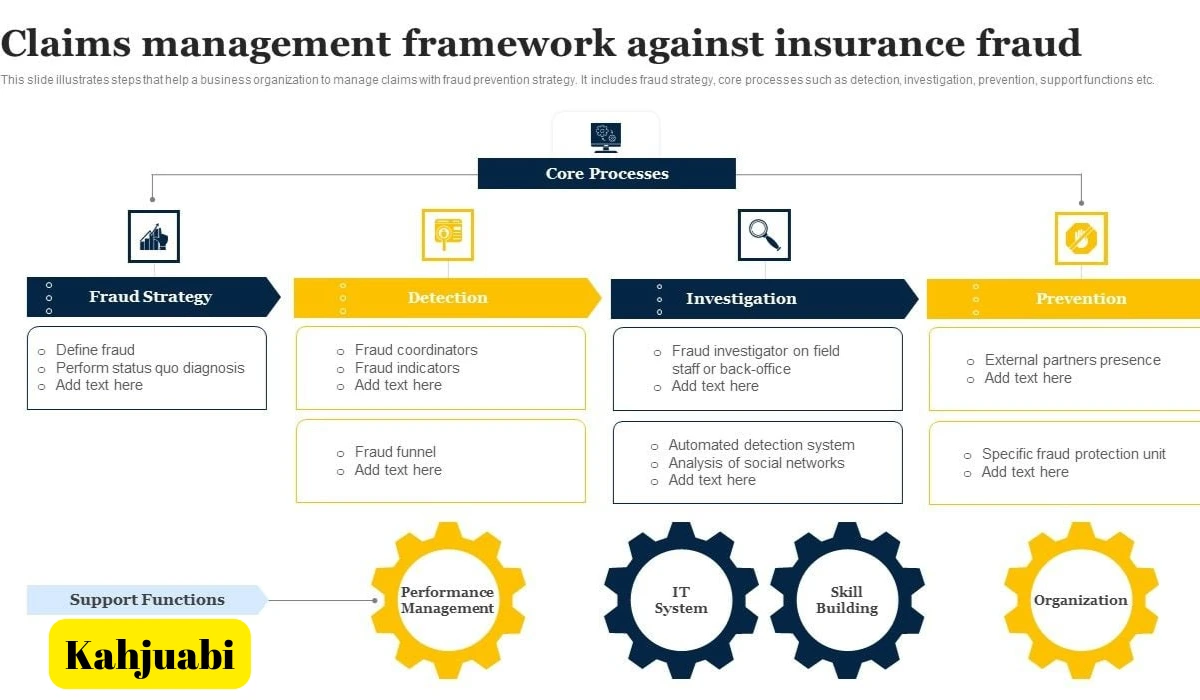

Kahjuabi represents a comprehensive insurance claims assistance service framework that originated in Estonia and has expanded across Northern Europe’s advanced InsurTech ecosystems. The Estonian term “kahjuabi” translates directly to “damage assistance” or “claims help,” describing 24/7 support services that activate immediately following accidents, property damage, or loss events. Multiple Estonian insurance providers including LHV, FS Kindlustus, and IIZI offer kahjuabi services through dedicated hotlines like 680 1122 and 666 0300, providing policyholders with immediate guidance on documentation, emergency repairs, and claims navigation rather than waiting for traditional adjuster assessments that can take days or weeks.

The kahjuabi model fundamentally differs from conventional claims processing by prioritizing proactive intervention over reactive compensation. Traditional insurance operates on delayed indemnification where policyholders submit claims, wait for adjuster evaluations, and eventually receive reimbursement after the damage has already occurred and potentially worsened. Kahjuabi services deploy expert assistance to incident sites within hours, offering real-time advice on damage mitigation, coordinating emergency services, and handling documentation requirements while events are still unfolding. Estonian providers typically bundle kahjuabi with motor vehicle insurance policies for approximately 0.99 euros monthly, automatically extending coverage for the entire policy period, making immediate claims support accessible to average consumers rather than limiting it to premium-tier customers.

The service operates on three critical pillars that distinguish it from standard insurance support. Ubiquity ensures accessibility across borders and time zones, particularly valuable for logistics companies and international travelers whose incidents rarely occur in convenient jurisdictions. Expertise means kahjuabi providers employ legal specialists and engineers capable of making technical assessments on-site rather than relying on generalist call center staff. Autonomy grants assistance teams authority to authorize emergency spending or immediate repairs without waiting for multi-level corporate approval processes that traditionally delay recovery. These elements combine to address the fundamental gap between an accident occurring and a claim being finalized, reducing what industry analysts identify as “secondary loss” where initial minor damage escalates into catastrophic financial burdens due to delayed response.

The business case for kahjuabi services centers on downtime reduction rather than claims cost savings. In manufacturing or transport sectors, a 48-hour delay in claims processing can generate six-figure revenue losses as operations remain suspended pending insurance resolution. By deploying expert advocates immediately, companies bypass bureaucratic friction that typically stalls recovery, returning to normal operations days or weeks faster than traditional claims pathways allow. This competitive advantage has driven global adoption of what providers now term “Claims Assistance as a Service” models, expanding beyond motor and property insurance into professional liability, cyber-risk, and maritime insurance where post-incident complexity reaches its highest levels and rapid expert intervention provides maximum value.

The kahjuabi framework faces scalability challenges as demand for human-centric crisis support conflicts with operational efficiency requirements. Providing high-level expert advocacy around the clock across multiple jurisdictions demands significant resource investment that smaller insurance providers struggle to maintain profitably. While artificial intelligence and automated claims processing successfully streamline simple losses involving clear liability and straightforward damage assessments, the core value proposition of kahjuabi remains fundamentally human. People experiencing crisis situations require sophisticated advocates who understand emotional context and can navigate ambiguous situations, not merely efficient algorithms that process standardized scenarios. Industry observers note that as providers integrate AI capabilities, they must carefully balance automation efficiency against the risk of widening the “empathy gap” during vulnerable moments when policyholders most need personalized human support.

The evolution of kahjuabi from a regional Estonian service model to a global insurance innovation reflects broader shifts in consumer expectations and competitive dynamics. Companies increasingly select insurance providers based on assistance network robustness rather than simply comparing premium costs, signaling what analysts describe as the “de-commoditization” of insurance products. In high-risk sectors, comprehensive kahjuabi frameworks contribute to Environmental, Social, and Governance strategies by demonstrating organizational commitment to rapid recovery and stakeholder protection beyond basic contractual indemnification. As the model continues expanding internationally, the central tension remains between scaling immediate expert intervention to meet growing demand while preserving the personalized advocacy that distinguishes kahjuabi from traditional claims processing and justifies its premium positioning in competitive insurance markets.